How to Open a High-Interest Savings Account in Dublin

Introduction

In today’s uncertain economic climate, building a strong financial foundation is more important than ever. Whether you are a student, a working professional, a business owner, or a family living in Dublin, having a secure place to save your money can help you achieve long-term financial stability. One of the smartest ways to grow your savings safely is by opening a high-interest savings account.

High-interest savings accounts are becoming increasingly popular in Dublin because they provide better returns compared to standard savings accounts. With inflation, rising living costs, and fluctuating financial markets, many people are looking for safer financial strategies that allow their money to grow steadily without unnecessary risk.

Dublin, as the financial hub of Ireland, offers a wide range of banking options for savers. Traditional banks, digital banks, credit unions, and online financial institutions are all competing to attract customers by offering attractive interest rates, flexible account features, and convenient online banking tools.

This comprehensive guide explains everything you need to know about opening a high-interest savings account in Dublin. From understanding interest rates and comparing banks to learning about eligibility requirements and avoiding hidden fees, this article will help you make informed financial decisions while maximizing your savings potential.

What Is a High-Interest Savings Account?

A high-interest savings account is a type of bank account designed to help individuals grow their savings faster through competitive interest rates. Unlike regular savings accounts that often provide minimal returns, high-interest accounts offer significantly better annual percentage yields (APY).

These accounts are ideal for:

- Emergency funds

- Vacation savings

- House deposits

- Education funds

- Retirement preparation

- Business cash reserves

- Long-term financial goals

The main advantage is that your money earns interest while remaining relatively accessible. This makes high-interest savings accounts one of the safest and most flexible financial products available in Ireland.

In Dublin, many banks offer variable or fixed interest savings products. Variable-rate accounts may fluctuate depending on economic conditions, while fixed-rate accounts lock your money for a specific period in exchange for higher returns.

Why Dublin Residents Are Choosing High-Interest Savings Accounts

Rising Cost of Living

Dublin has experienced significant increases in housing, transportation, utilities, and food prices over recent years. As expenses rise, many residents are searching for ways to protect the value of their savings.

A high-interest savings account helps offset inflation by allowing savers to earn more on deposited funds.

Financial Security

Economic uncertainty encourages people to prioritize emergency savings. A strong savings account can provide peace of mind during unexpected situations such as:

- Job loss

- Medical emergencies

- Business downturns

- Home repairs

- Family emergencies

Low-Risk Investment Alternative

Not everyone wants to invest in stocks, cryptocurrency, or volatile assets. High-interest savings accounts provide a safer alternative with predictable returns and minimal risk.

Easy Online Banking Access

Modern banking technology makes it easier than ever to manage savings accounts online. Most banks in Dublin now provide:

- Mobile apps

- Online transfers

- Digital account opening

- Automated savings tools

- Spending analytics

- Instant notifications

Benefits of Opening a High-Interest Savings Account

1. Higher Returns on Savings

The biggest advantage is the ability to earn more interest compared to standard accounts. Over time, compound interest can significantly increase your savings balance.

For example, if you deposit €10,000 into a high-interest account with a competitive annual rate, your money grows steadily without requiring additional investment risks.

2. Safe and Secure Savings

Most reputable banks in Ireland are regulated and protected under financial protection schemes. This means your deposits are generally safeguarded up to certain limits.

3. Flexible Access to Funds

Many savings accounts allow quick withdrawals while still earning interest. This flexibility is useful for emergencies or planned financial goals.

4. Encourages Better Financial Habits

Having a dedicated savings account motivates individuals to budget carefully and build consistent saving habits.

5. Suitable for All Income Levels

Whether you save €50 or €5,000 per month, high-interest accounts can help your money grow efficiently.

Types of High-Interest Savings Accounts in Dublin

Instant Access Savings Accounts

These accounts allow you to withdraw funds whenever needed while earning competitive interest.

Best for:

- Emergency savings

- Short-term goals

- Flexible cash management

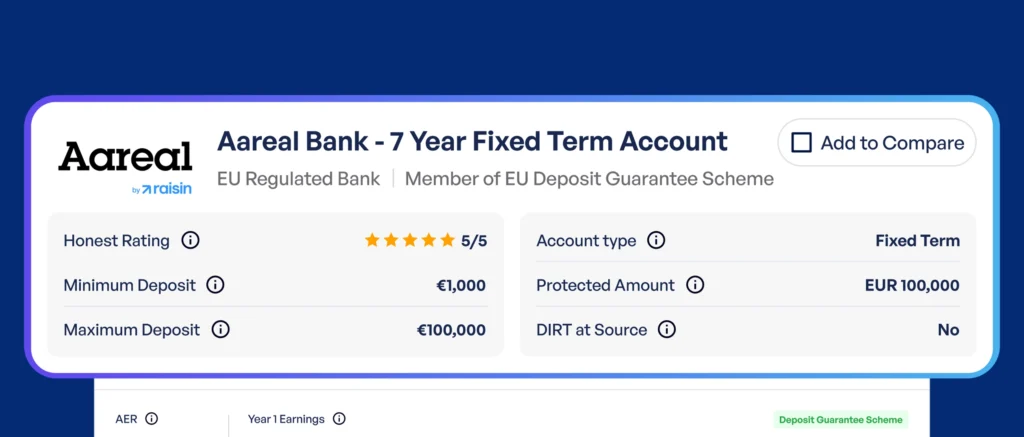

Fixed-Term Deposit Accounts

Fixed-term accounts lock your money for a specific duration, usually between six months and five years.

Benefits include:

- Higher interest rates

- Guaranteed returns

- Stable savings growth

However, withdrawing early may result in penalties.

Online Savings Accounts

Digital-only banks often offer higher rates because they have lower operating costs.

Advantages include:

- Better interest rates

- Lower fees

- Fast account setup

- Mobile banking convenience

Credit Union Savings Accounts

Credit unions in Dublin provide community-focused savings options with competitive rates and personalized customer service.

How Interest Rates Work

Understanding interest rates is essential when choosing a savings account.

Annual Percentage Yield (APY)

APY represents the total amount of interest earned in one year, including compound interest.

Compound Interest

Compound interest allows you to earn interest on both your original deposit and previously earned interest.

This creates exponential savings growth over time.

Variable vs Fixed Interest Rates

Variable Rates

- Can increase or decrease

- Flexible access

- Influenced by market conditions

Fixed Rates

- Locked for a set period

- Predictable returns

- Usually higher than variable accounts

Key Factors to Consider Before Opening an Account

Interest Rate Comparison

Always compare rates between different financial institutions.

Even a small percentage difference can significantly impact long-term earnings.

Minimum Deposit Requirements

Some banks require minimum opening balances.

Others allow accounts with no minimum deposit.

Withdrawal Restrictions

Check whether the account limits:

- Number of withdrawals

- Transfer amounts

- Early access penalties

Banking Fees

Avoid accounts with excessive:

- Monthly maintenance fees

- Transaction fees

- Withdrawal charges

- Dormancy fees

Online Banking Features

Choose a bank with reliable digital tools such as:

- Mobile apps

- Budget tracking

- Automatic transfers

- Real-time alerts

Customer Support Quality

Responsive customer service is crucial for resolving issues quickly.

Documents Needed to Open a High-Interest Savings Account in Dublin

Most banks in Dublin require the following documents:

Proof of Identity

Accepted documents may include:

- Passport

- Irish driving license

- National ID card

Proof of Address

Common examples include:

- Utility bills

- Bank statements

- Rental agreements

- Government correspondence

Personal Public Service Number (PPSN)

Some institutions may request your PPSN for tax and identification purposes.

Proof of Income

Certain banks may ask for:

- Payslips

- Employment contracts

- Tax returns

- Business income records

Step-by-Step Guide to Opening a High-Interest Savings Account in Dublin

Step 1: Define Your Savings Goals

Determine why you want to save money.

Examples include:

- Buying a home

- Creating an emergency fund

- Paying for education

- Starting a business

- Retirement planning

Your financial goals help determine the best type of account.

Step 2: Compare Banks and Financial Institutions

Research multiple providers before making a decision.

Look at:

- Interest rates

- Fees

- Customer reviews

- Online banking features

- Withdrawal flexibility

- Deposit insurance protections

Step 3: Prepare Your Documents

Gather all required identification and financial documents in advance.

This speeds up the application process.

Step 4: Submit Your Application

Most banks in Dublin allow applications through:

- Online banking platforms

- Mobile apps

- Local branches

- Video verification systems

Step 5: Verify Your Identity

Banks must comply with anti-money laundering regulations.

You may need to:

- Upload documents

- Attend an in-person appointment

- Complete video verification

Step 6: Deposit Funds

Once approved, transfer money into your new savings account.

Some banks allow:

- Bank transfers

- Debit card deposits

- Salary transfers

- Cash deposits

Step 7: Activate Online Banking

Set up:

- Mobile banking

- Password protection

- Two-factor authentication

- Savings alerts

This ensures convenient and secure account management.

Best Features to Look for in Dublin Savings Accounts

Competitive Interest Rates

High returns remain the most important factor.

Strong Mobile Banking Apps

Modern savers prefer digital convenience.

A good app should provide:

- Fast transfers

- Spending insights

- Account alerts

- Savings automation

No Hidden Charges

Transparent banking is essential.

Always read terms and conditions carefully.

Flexible Access

Choose accounts that balance strong interest with reasonable access to funds.

Excellent Reputation

Well-established banks with strong customer reviews often provide better service reliability.

Common Mistakes to Avoid

Ignoring Fees

Some accounts advertise attractive interest rates but include hidden charges that reduce profits.

Not Reading Terms Carefully

Always review:

- Withdrawal policies

- Interest conditions

- Bonus rate requirements

- Account maintenance rules

Choosing the First Offer Available

Comparing multiple institutions can help you secure better returns.

Leaving Large Balances in Low-Interest Accounts

Many people lose potential earnings by keeping money in outdated accounts with minimal interest.

Forgetting About Taxes

Interest earned may be subject to taxation in Ireland.

Understand your obligations before opening an account.

Online Banks vs Traditional Banks in Dublin

Traditional Banks

Advantages:

- Physical branches

- Face-to-face support

- Established reputation

- Broad financial services

Disadvantages:

- Lower interest rates

- Higher fees

- Slower innovation

Online Banks

Advantages:

- Higher interest rates

- Lower operating costs

- User-friendly technology

- Faster account setup

Disadvantages:

- Limited physical support

- Fully digital communication

- Potential service delays during technical issues

How to Maximize Your Savings Growth

Automate Monthly Deposits

Automatic transfers help maintain consistent saving habits.

Reduce Unnecessary Spending

Track expenses and eliminate non-essential purchases.

Use Budgeting Apps

Digital budgeting tools help identify saving opportunities.

Reinvest Earned Interest

Allowing compound interest to accumulate can dramatically increase long-term growth.

Monitor Interest Rates Regularly

Banks frequently adjust rates.

Review your account annually to ensure competitive returns.

Emergency Funds and Financial Stability

Financial experts recommend maintaining an emergency fund covering at least three to six months of expenses.

A high-interest savings account is ideal for emergency funds because it combines:

- Security

- Accessibility

- Steady growth

Dublin residents facing high living expenses can benefit greatly from strong emergency savings.

Saving for a House Deposit in Dublin

Property prices in Dublin remain among the highest in Ireland.

Building a house deposit requires disciplined saving strategies.

High-interest savings accounts help future homeowners:

- Protect savings safely

- Earn additional interest

- Separate housing funds from daily spending

- Reach financial goals faster

Many first-time buyers use dedicated savings accounts to prepare for mortgage applications.

Business Savings Accounts in Dublin

Entrepreneurs and small business owners also benefit from high-interest business savings accounts.

Advantages include:

- Better cash flow management

- Emergency business reserves

- Tax preparation funds

- Expansion savings

- Financial stability during slow periods

Dublin’s growing startup ecosystem has increased demand for flexible business banking solutions.

Student Savings Strategies in Dublin

Students studying in Dublin often face:

- Rising rent costs

- Tuition fees

- Transportation expenses

- Food inflation

A high-interest savings account can help students:

- Build financial discipline

- Save for future opportunities

- Reduce financial stress

- Create emergency funds

Some banks also offer student-friendly accounts with lower fees.

Digital Banking Trends in Ireland

Ireland’s banking sector continues to evolve rapidly.

Popular digital trends include:

AI-Powered Financial Tools

Banks increasingly use artificial intelligence to provide:

- Spending analysis

- Personalized savings recommendations

- Fraud detection

- Financial forecasting

Mobile-First Banking

Many consumers now manage finances entirely through smartphones.

Contactless Payments

Cashless transactions continue to dominate daily banking activities.

Open Banking Integration

Open banking technology allows customers to connect multiple financial accounts into one platform.

Security Tips for Online Savings Accounts

Use Strong Passwords

Avoid weak passwords and update them regularly.

Enable Two-Factor Authentication

Additional verification significantly improves account security.

Monitor Transactions Frequently

Review account activity to detect suspicious behavior early.

Avoid Public Wi-Fi for Banking

Use secure internet connections when accessing financial accounts.

Beware of Phishing Scams

Never share banking information through suspicious emails or messages.

Tax Considerations for Savings Accounts in Ireland

Interest earned from savings may be subject to Deposit Interest Retention Tax (DIRT) in Ireland.

Important points include:

- Banks may deduct taxes automatically

- Tax rates can change over time

- Certain exemptions may apply

- Accurate financial records are important

Consulting a financial advisor or tax professional can help optimize your savings strategy.

Future of High-Interest Savings Accounts in Dublin

The future of savings accounts in Ireland will likely include:

- More competitive digital banking

- Improved mobile technology

- AI-driven financial management

- Personalized savings tools

- Flexible hybrid banking services

As financial competition grows, consumers may benefit from improved interest rates and better customer experiences.

Why Financial Literacy Matters

Opening a high-interest savings account is only one part of long-term financial success.

Financial literacy helps individuals:

- Avoid debt problems

- Build wealth responsibly

- Plan retirement effectively

- Invest wisely

- Handle economic uncertainty

In Dublin’s fast-paced economy, strong financial knowledge can provide major long-term advantages.

Frequently Asked Questions

Can Non-Residents Open Savings Accounts in Dublin?

Some banks allow non-residents to open accounts, although additional documentation may be required.

Are Online Savings Accounts Safe?

Reputable regulated institutions generally provide strong security protections and deposit safeguards.

How Much Money Should I Keep in Savings?

Financial experts often recommend maintaining at least three to six months of living expenses.

Can I Have Multiple Savings Accounts?

Yes. Many people separate savings into categories such as:

- Emergency funds

- Travel savings

- House deposits

- Education funds

- Retirement planning

Is a Fixed-Term Account Better?

Fixed-term accounts may provide higher rates but reduce flexibility.

The best option depends on your financial goals.

Conclusion

Opening a high-interest savings account in Dublin is one of the smartest financial decisions you can make in today’s economy. Whether you are saving for a future home, building an emergency fund, preparing for retirement, or managing business finances, the right savings account can help your money grow securely and efficiently.

Dublin offers a wide variety of banking options, from traditional institutions to modern digital banks. By comparing interest rates, understanding account terms, avoiding hidden fees, and using smart savings strategies, you can maximize your financial growth while maintaining easy access to your funds.

The key to successful saving is consistency. Even small monthly contributions can grow substantially over time through compound interest. As Ireland’s financial sector continues evolving with advanced technology and competitive banking services, consumers now have more opportunities than ever to optimize their savings.

Take the time to research your options carefully, choose a trusted financial institution, and begin building a stronger financial future today. A well-managed high-interest savings account can provide stability, security, and peace of mind for years to come.