Understanding Taxes and Financial Responsibilities in Ireland

Ireland is widely recognized as one of Europe’s most dynamic economies, attracting professionals, entrepreneurs, and students from around the world. While the country offers many opportunities, understanding its tax system and financial responsibilities is essential for anyone living or working there. Whether you are an employee, self-employed, or running a business, having a clear grasp of how taxes work in Ireland can help you stay compliant, avoid penalties, and manage your finances more effectively.

Overview of the Irish Tax System

The Irish tax system is administered by the Office of the Revenue Commissioners, commonly known as Revenue. It operates on a self-assessment basis for certain taxpayers, while employees typically pay taxes through the Pay As You Earn (PAYE) system.

Ireland’s taxation system is relatively straightforward compared to many other countries, but it still requires careful attention to detail. Taxes collected by the government fund public services such as healthcare, education, infrastructure, and social welfare programs.

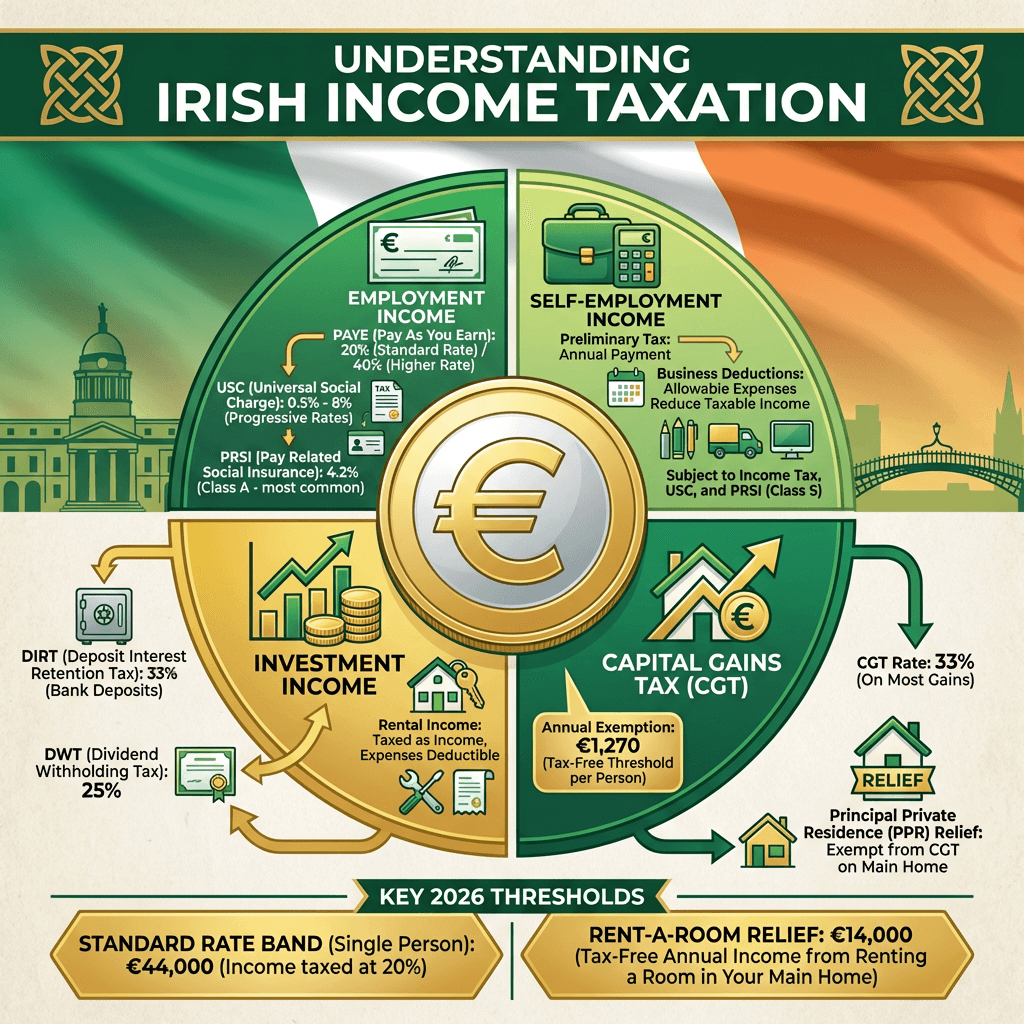

The main types of taxes individuals encounter in Ireland include income tax, Universal Social Charge (USC), and Pay Related Social Insurance (PRSI). Businesses may also be subject to corporation tax, value-added tax (VAT), and other levies.

Income Tax in Ireland

Income tax is the primary tax paid by individuals in Ireland. It is calculated based on your earnings and is charged at different rates depending on your income level.

Tax Rates

Ireland uses a progressive tax system, meaning that higher income levels are taxed at higher rates. There are two main tax bands:

- The standard rate (20%)

- The higher rate (40%)

The portion of your income that falls within the standard band is taxed at 20%, while income above that threshold is taxed at 40%. The exact thresholds vary depending on your personal circumstances, such as whether you are single, married, or a single parent.

Tax Credits

Tax credits reduce the amount of tax you have to pay. They are subtracted directly from your tax liability rather than your income. Common tax credits in Ireland include:

- Personal tax credit

- Employee tax credit

- Married person’s tax credit

Understanding and claiming the correct tax credits can significantly reduce your overall tax burden.

PAYE System for Employees

Most employees in Ireland pay their taxes through the PAYE system. Under this system, your employer deducts income tax, USC, and PRSI directly from your salary before you receive it.

This system simplifies tax compliance for employees, as it eliminates the need to file complex tax returns in most cases. However, employees should still review their tax records regularly to ensure accuracy and claim any additional credits or reliefs they are entitled to.

Universal Social Charge (USC)

The Universal Social Charge is a tax on gross income, meaning it is calculated before most deductions. USC applies to a wide range of income sources, including wages, self-employment income, and rental income.

USC is charged at different rates depending on income levels, with lower rates applied to lower incomes. Although it may seem like an additional burden, USC contributes to funding essential public services in Ireland.

Pay Related Social Insurance (PRSI)

PRSI is another mandatory contribution that funds social welfare benefits such as pensions, unemployment support, and illness benefits. Both employees and employers contribute to PRSI.

The amount you pay depends on your earnings and employment status. Paying PRSI ensures that you are eligible for various social protection benefits, making it an important part of financial planning in Ireland.

Tax Responsibilities for the Self-Employed

Self-employed individuals in Ireland have additional responsibilities compared to employees. They must register for self-assessment and file annual tax returns.

Self-Assessment System

Under self-assessment, individuals calculate their own tax liability and submit their returns to Revenue. This includes income tax, USC, and PRSI.

Preliminary Tax

Self-employed individuals are required to pay preliminary tax each year. This is an advance payment of your expected tax liability for the current year. Failure to pay sufficient preliminary tax can result in interest charges.

Record Keeping

Maintaining accurate financial records is essential for self-employed individuals. This includes keeping track of income, expenses, invoices, and receipts. Proper record-keeping ensures accurate tax reporting and helps avoid issues with Revenue.

Value-Added Tax (VAT)

VAT is a consumption tax applied to goods and services in Ireland. Businesses that exceed certain turnover thresholds must register for VAT.

VAT Rates

Ireland has several VAT rates, including:

- Standard rate (23%)

- Reduced rate (13.5%)

- Lower rate (9%) for specific sectors such as tourism and hospitality

Businesses collect VAT from customers and remit it to Revenue. They can also reclaim VAT on business-related expenses.

Corporation Tax

Ireland is known for its competitive corporation tax rate, which has attracted many multinational companies. The standard corporation tax rate is 12.5% on trading income.

Companies must file annual corporation tax returns and comply with strict reporting requirements. While the low tax rate is appealing, businesses must ensure they meet all regulatory obligations.

Other Financial Responsibilities

In addition to taxes, individuals and businesses in Ireland have other financial responsibilities that are important for maintaining financial stability.

Budgeting and Financial Planning

Managing your income and expenses effectively is crucial. Creating a budget helps you track your spending, save money, and prepare for future expenses.

Pension Contributions

Planning for retirement is an essential financial responsibility. Contributing to a pension scheme not only secures your future but may also provide tax relief.

Insurance

Having adequate insurance coverage, such as health insurance, car insurance, and home insurance, is important for protecting yourself against unexpected events.

Compliance with Regulations

Businesses must comply with various financial and legal regulations, including maintaining proper accounts, filing returns on time, and adhering to employment laws.

Common Mistakes to Avoid

Understanding the tax system can help you avoid common pitfalls.

1. Failing to Register with Revenue

New employees or self-employed individuals must ensure they are registered with Revenue. Failure to do so can lead to incorrect tax deductions or penalties.

2. Missing Deadlines

Late tax filings or payments can result in interest charges and penalties. Keeping track of important dates is essential.

3. Incorrect Claims

Claiming incorrect tax credits or deductions can lead to audits and fines. Always ensure your claims are accurate and supported by documentation.

4. Poor Record Keeping

Inadequate records can cause problems during tax assessments. Keeping organized and detailed records is crucial.

Tips for Managing Taxes Effectively

Here are some practical tips to help you manage your taxes and financial responsibilities in Ireland:

- Stay informed about tax laws and updates

- Use online tools provided by Revenue to manage your tax affairs

- Seek professional advice if you have complex financial situations

- Plan ahead for tax payments to avoid financial strain

- Keep all financial documents organized and accessible

The Role of Technology in Tax Management

Technology has made it easier to manage taxes in Ireland. Revenue’s online platform allows individuals and businesses to file returns, track payments, and access important information.

Digital tools and accounting software can also simplify financial management, especially for self-employed individuals and small businesses. These tools help automate processes, reduce errors, and improve efficiency.

Conclusion

Understanding taxes and financial responsibilities in Ireland is essential for anyone living or working in the country. From income tax and USC to VAT and corporation tax, each component plays a role in supporting public services and the economy.

While the system may seem complex at first, taking the time to learn and stay organized can make a significant difference. Whether you are an employee, self-employed, or a business owner, being proactive about your financial responsibilities will help you avoid problems and achieve greater financial stability.

Ultimately, managing your taxes effectively is not just about compliance—it is about making informed decisions that support your long-term financial well-being. By staying informed, planning ahead, and seeking guidance when needed, you can navigate Ireland’s tax system with confidence and ease.